F-1 Visa Students from New Zealand Face Unique Banking Hurdles

F-1 visa students from New Zealand often need a U.S. bank account for practical reasons related to their studies or potential U.S. employment. Unlike U.S. residents, you cannot simply walk into a branch with your passport. Most U.S. banks have strict Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations that make opening an account remotely, especially for non-residents, challenging. This is particularly true if you do not have a U.S. address or a Social Security Number (SSN). The primary friction point is the requirement for a physical U.S. presence and verifiable U.S. identification, which most F-1 students lack initially. Without a U.S. bank account, managing funds for living expenses, tuition payments, or any part-time work can become complex and costly due to international transfer fees and currency conversion rates.

When a U.S. Bank Account Becomes Necessary for F-1 Students

A U.S. bank account is often required for F-1 visa students due to U.S. tax obligations. While your primary purpose is study, certain activities can trigger U.S. tax filing requirements. For instance, if you engage in authorized practical training, such as Optional Practical Training (OPT) or Curricular Practical Training (CPT), you will likely have U.S. source income. This income necessitates filing U.S. tax returns, such as Form 1040-NR (U.S. Nonresident Alien Income Tax Return). Additionally, F-1 students are generally considered U.S. tax residents for the purpose of filing Form 8843, even if they have no U.S. income, to report their presence in the U.S. as a student. Some students may also have U.S. scholarship or fellowship grants that require reporting. Managing these financial obligations and potential treaty benefits, especially if claiming exemptions under the U.S.-New Zealand tax treaty, is significantly easier with a U.S. bank account for receiving payments and making tax remittances.

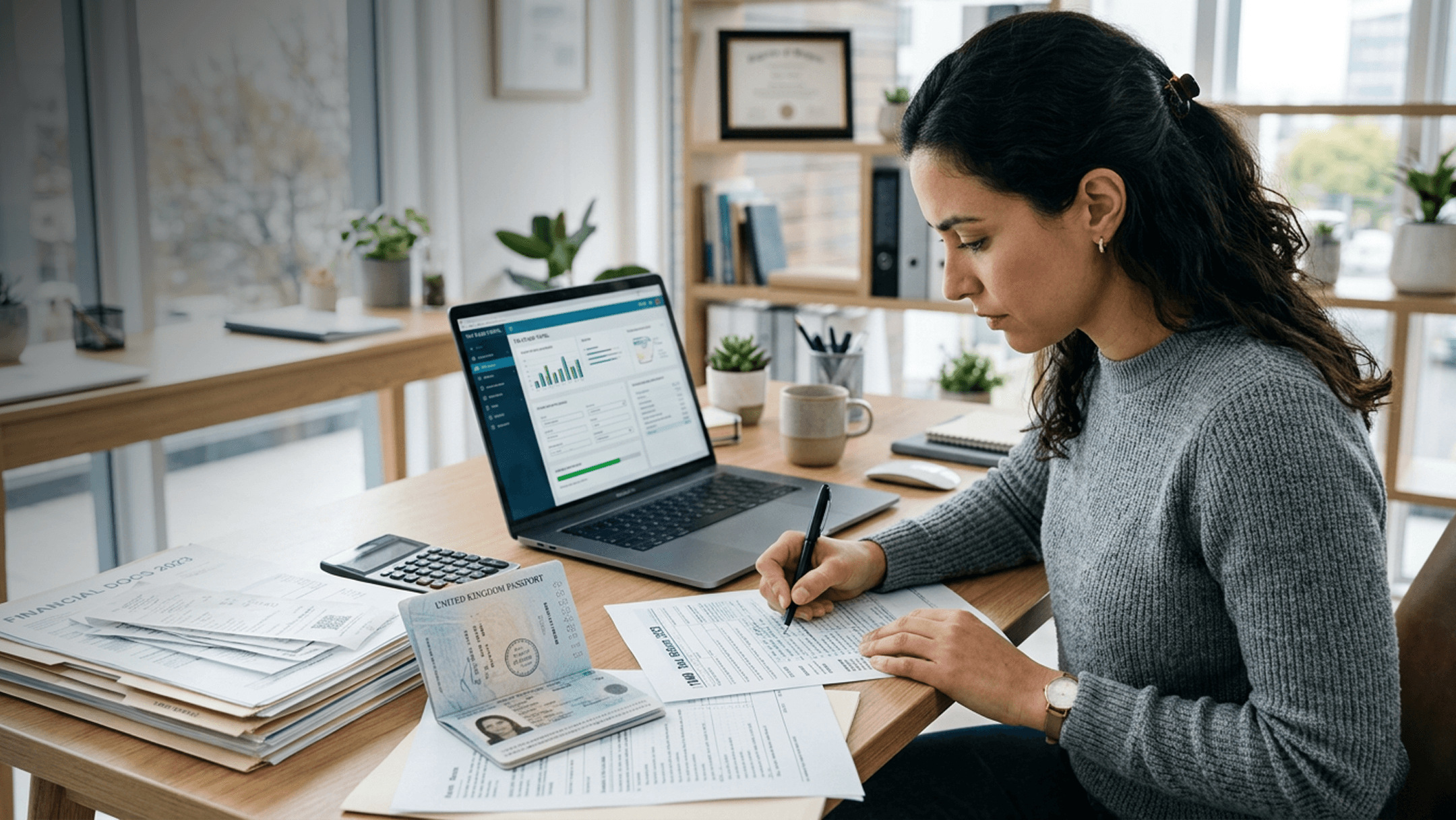

Essential Documentation for Opening Your U.S. Bank Account

Opening a U.S. bank account as a non-resident requires specific documentation. The exact requirements vary by bank, but generally include a valid passport as primary identification. You will also need proof of address, which can be from New Zealand, such as a utility bill or bank statement. If you are opening a business account (which may be relevant if you are undertaking entrepreneurial activities or certain types of employment), you will need an Employer Identification Number (EIN) confirmation letter, often obtained by filing Form SS-4 with the IRS. Other business documents might include Articles of Organization or a similar formation document if you have established a U.S. entity like a U.S. LLC. For personal accounts, the process is typically simpler but still requires robust identification. Some institutions may request a U.S. mailing address, even if it's a virtual one provided by a service. All documentation must be clear, legible, and up-to-date. It is critical to ensure that names and addresses match across all submitted documents to avoid delays or rejections.

The Remote U.S. Bank Account Application Process

The process for opening a U.S. bank account remotely typically takes 5–10 business days from the submission of a complete application to account activation. It begins with selecting a bank or financial institution that supports non-resident account opening. Many traditional large banks do not offer this service, so fintech solutions or specialized banking partners are often the best route. You will complete an online application, providing all the necessary personal and/or business details. This is followed by submitting the required documents electronically. Banks then conduct their KYC/AML checks. If approved, you will receive account details, and a debit card will be mailed to your provided address, which can be in New Zealand. The entire process is designed to be completed without a physical visit to a U.S. branch.itin.net assists clients in navigating this process, connecting them with suitable banking partners and ensuring all application requirements are met efficiently.

Common Pitfalls for F-1 Students from New Zealand

F-1 visa students from New Zealand commonly encounter specific pitfalls when attempting to open a U.S. bank account. A major issue is applying to banks that outright reject non-resident applications; many prominent U.S. banks are not equipped for remote international account openings. Another frequent mistake is incomplete or mismatched documentation. For instance, using a different name on your passport than on other submitted forms can lead to immediate rejection. Some students underestimate the need for an EIN if their activities necessitate business banking, even if they are operating as a sole proprietor. Attempting to open an account without understanding the bank's specific requirements for non-residents, particularly regarding proof of address or the need for a U.S. taxpayer identification number (like an ITIN, though not always required for the bank itself, it can be useful for tax filings), can also cause significant delays. Ensure you have a clear understanding of the bank's policy on non-resident accounts before starting the application.

Leveraging the Certified Acceptance Agent (CAA) Path

For individuals requiring an ITIN to fulfill U.S. tax obligations, the path through a Certified Acceptance Agent (CAA) offers a streamlined approach. A CAA, like itin.net, is authorized by the IRS to assist taxpayers in obtaining an ITIN. While not directly involved in bank account opening, the CAA process ensures your identity documents are verified correctly, which can be a prerequisite for certain banking services or for accurately completing tax forms that might be requested by banks indirectly. The benefit of using a CAA for your ITIN application is the verification of your identification documents without needing to mail originals to the IRS. This verified identity can then be more readily accepted by financial institutions when opening accounts or establishing financial relationships in the U.S. The CAA’s role is to ensure that the documentation submitted for an ITIN is accurate and complete, reducing the chances of errors that could impact future financial dealings.

Next Steps for Securing Your U.S. Banking

After understanding the requirements and process, the next logical step is to identify a suitable U.S. financial institution. Review the options available for non-residents and compare their services, fees, and account opening procedures. If you anticipate U.S. tax filing obligations or need an ITIN for other reasons, initiating that process concurrently can be beneficial. For instance, if you need an ITIN, you can begin the application process. Consider consulting with a specialist at itin.net to discuss your specific situation and determine the most efficient path forward for both your ITIN and U.S. bank account needs. You can review our U.S. bank account opening services or contact us for personalized guidance.

Practical tips

- Use the same legal name across all application documents, including your passport and any proof of address. Mismatched names are a common reason for application rejection.

- Gather all required documents before starting the application. This includes clear copies of your passport, proof of address in New Zealand, and potentially an EIN confirmation letter if you require a business account.

- Confirm the bank's policy on non-resident accounts. Some institutions have specific requirements or limitations for individuals living outside the U.S.

- If you need an ITIN for U.S. tax purposes, begin that application process early, as it can sometimes be a prerequisite or helpful supporting document for financial institutions.

- Be prepared for a verification call or email from the bank. Respond promptly to any requests for additional information to avoid delaying the account opening process.

Frequently asked questions

Can I open a U.S. bank account from New Zealand without visiting the U.S.?

Yes, many fintech companies and some traditional banks allow non-residents to open U.S. bank accounts remotely from New Zealand. The process involves online applications and electronic submission of documents.

Do I need a U.S. address to open a bank account?

Some banks require a U.S. mailing address, which can sometimes be a virtual address provided by a mail forwarding service. Other institutions may accept your New Zealand address as proof of residency.

What is an EIN and do I need one for a personal U.S. bank account?

An EIN (Employer Identification Number) is like a Social Security Number for businesses, issued by the IRS. You typically do not need an EIN for a personal U.S. bank account, but you will need one if you are opening a business account or operating as a U.S. business entity.

How long does it take to open a U.S. bank account from New Zealand?

The typical timeline for opening a U.S. bank account remotely is 5–10 business days from the time your application and all required documents are submitted and approved.

Will my F-1 visa status affect my ability to open a U.S. bank account?

Your F-1 visa status itself does not typically prevent you from opening a U.S. bank account. The primary factors are your non-resident status and the documentation you can provide, as per the bank's KYC/AML policies.

Do I need an ITIN to open a U.S. bank account?

An ITIN (Individual Taxpayer Identification Number) is generally not a requirement for opening a personal U.S. bank account. However, if you have U.S. tax filing obligations, you will need an ITIN or SSN, and having one can sometimes assist with the banking application process.