OPT Workers from Niger Face Unique Banking Hurdles

OPT workers from Niger specifically encounter challenges opening a U.S. bank account due to their non-resident status and the specific requirements of U.S. financial institutions. Unlike U.S. residents or citizens, you cannot simply walk into a branch with a passport and proof of address. Most traditional U.S. banks have strict Know Your Customer (KYC) and Anti-Money Laundering (AML) policies that make it difficult, if not impossible, for non-residents without a U.S. physical presence or established U.S. credit history to open an account remotely. This is particularly true for individuals based in Niger, where direct access to U.S. banking infrastructure is limited. The process often requires navigating a complex application system designed primarily for U.S. persons, leading to frequent rejections for those outside these parameters. Identifying financial institutions that cater to international clients and understanding their specific documentation requirements is the first critical step for any OPT worker from Niger seeking U.S. banking services. This often means looking beyond the large national banks to fintech solutions or specialized providers designed for non-residents. The goal is to find a service that can accommodate your unique situation as an OPT worker based abroad.

When You Need a U.S. Bank Account as an OPT Worker

For OPT workers from Niger, a U.S. bank account is often a necessity driven by the nature of their employment and academic status in the United States. While not always mandated by U.S. immigration law itself, many U.S. employers, particularly those offering stipends, salaries, or reimbursement for expenses, will require a U.S. bank account for direct deposit. This simplifies payroll processing for the employer and ensures timely access to funds for you. Furthermore, certain U.S.-based platforms or services you might use for professional development, online courses, or even some freelance opportunities may require a U.S. financial account for transactions. While some platforms might accept international accounts, many prefer or require a domestic U.S. account for ease of use and compliance. The critical trigger is often an offer of employment or an internship that necessitates receiving U.S. dollar compensation. Without a U.S. bank account, you might face delays in payment, additional conversion fees, or be unable to accept certain job offers altogether. Therefore, securing a U.S. bank account should be a priority once you have a confirmed OPT position.

Required Documents for Non-Residents

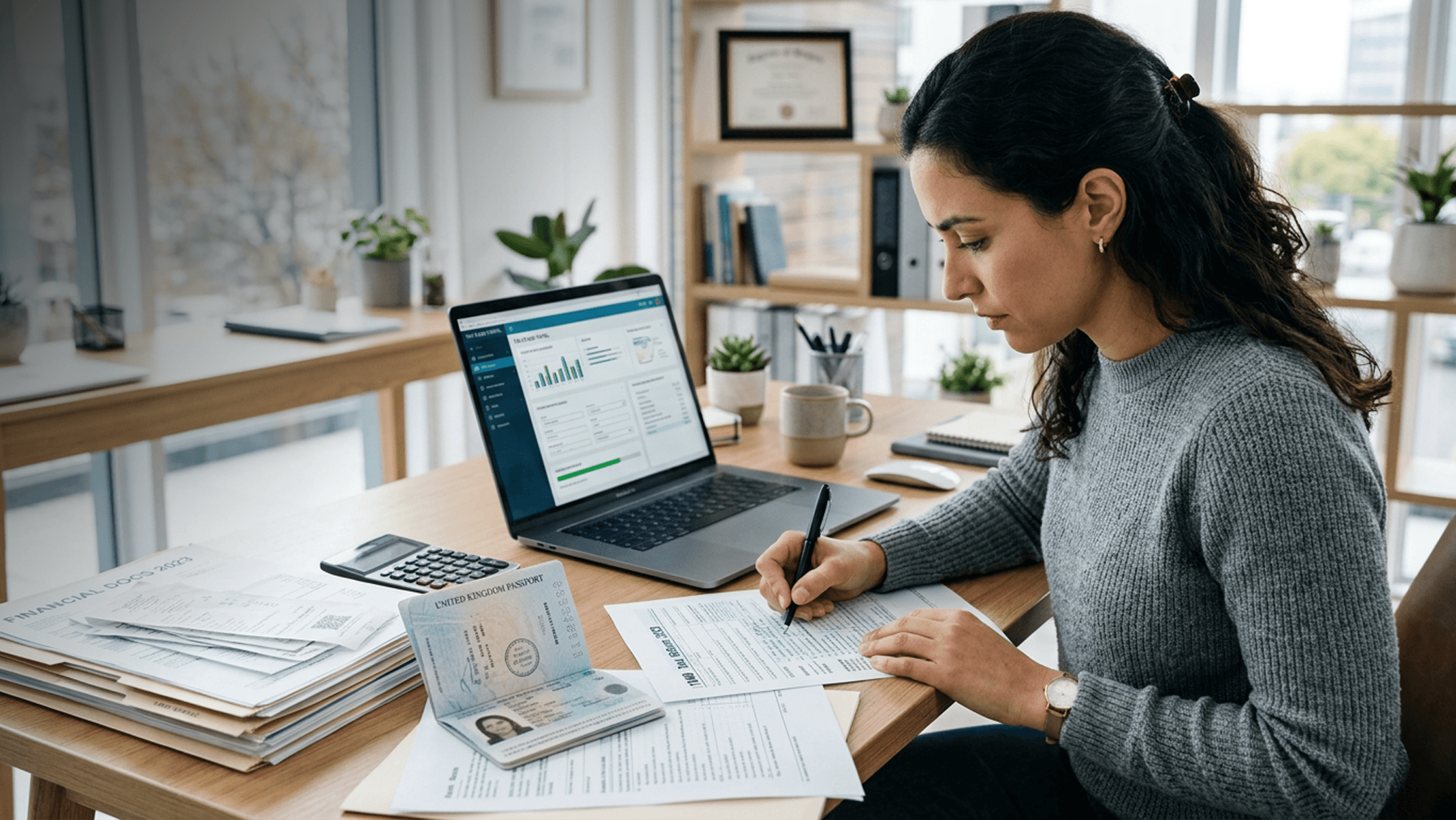

Opening a U.S. bank account remotely as an OPT worker from Niger requires a specific set of documents tailored to non-resident applicants. The exact requirements vary by institution, but common documents include a valid passport, which serves as your primary identification. You will also need proof of your U.S. address, typically a utility bill or lease agreement. Some institutions may request proof of your U.S. visa status or your Employment Authorization Document (EAD) to confirm your eligibility to work and reside in the U.S. for a period. For business accounts, which many OPT workers may need if operating independently or engaging in freelance work, an Employer Identification Number (EIN) is essential. This is obtained by filing Form SS-4 with the IRS. Additionally, you might need formation documents like Articles of Organization if you are establishing a U.S. LLC. Some banks might also ask for a utility bill from your Nigerien address to verify your foreign residency. It is crucial to have all these documents ready and accurately translated if they are not in English. Mismatched information or missing documents are primary reasons for application denial.

The Remote Application Process for OPT Workers

The process of opening a U.S. bank account remotely for OPT workers from Niger typically begins with identifying a financial institution that supports non-resident applications. Many large U.S. banks do not offer this service, so exploring fintech alternatives like Mercury, Relay, or Brex, or banks with specific international client programs is often necessary. Once a suitable institution is found, you will complete an online application form. This application is bank-specific and designed to comply with U.S. financial regulations, including KYC and AML checks. You will be prompted to upload scanned copies of your required documents, such as your passport, proof of U.S. address, and potentially your EAD or ITIN. If you are applying for a business account, you will also need to submit your EIN confirmation letter and any business formation documents. The review process by the bank can take anywhere from 5 to 10 business days. During this time, the bank verifies your identity and documentation. If approved, you will be notified, and your debit card and account details will be mailed to your U.S. address. This timeline can be slightly longer depending on the thoroughness of the bank's verification and any additional information they might request.

Common Pitfalls for OPT Workers from Niger

OPT workers from Niger often fall into specific traps when trying to open a U.S. bank account. A significant pitfall is applying to banks that outright refuse non-resident applicants, wasting valuable time and effort. Many assume any U.S. bank will accommodate them, not realizing the stringent policies of most national banks. Another common mistake is failing to provide complete and accurate documentation. This includes using a name on the application that doesn't precisely match your passport or other official documents, or submitting blurry or incomplete scans. For those needing a business account, attempting to open one without first securing an EIN is a frequent error. Banks require proof of a registered U.S. business entity, and an EIN is a fundamental part of that. Additionally, some OPT workers may overlook the need for a U.S. physical address for receiving account statements and debit cards. Relying solely on a foreign address will likely lead to rejection. Understanding these specific challenges before starting the application is key to a successful outcome.

The Certified Acceptance Agent (CAA) Advantage

For OPT workers from Niger, navigating the complexities of U.S. financial and tax documentation can be daunting. This is where the role of a Certified Acceptance Agent (CAA) becomes particularly valuable. A CAA, like those at itin.net, is an individual or entity authorized by the IRS to assist taxpayers in obtaining an ITIN. While the primary function is ITIN application assistance, CAAs often provide broader support for non-residents dealing with U.S. financial matters. They can help ensure that your documentation, such as your passport and other identification, is properly verified and certified. This certification can sometimes streamline applications with financial institutions that recognize the validity of a CAA's certification. For instance, when applying for an ITIN, a CAA can review your original documents and send certified copies to the IRS, avoiding the need to mail your original passport. This level of assurance and accuracy in documentation verification can translate into a smoother overall process when applying for a U.S. bank account, as it demonstrates a thorough approach to compliance and identity verification. Utilizing a CAA ensures your application is handled with expertise, reducing the risk of errors that could lead to delays or rejections.

Next Steps for Establishing U.S. Banking

Once you have successfully opened your U.S. bank account, the next steps involve managing it effectively and ensuring compliance with any ongoing requirements. Activate your debit card immediately and set up online banking access. Familiarize yourself with the bank's mobile app and transaction monitoring features. If you opened a business account, ensure you understand any reporting requirements associated with it, such as Form 5472 for foreign-owned U.S. disregarded entities, which is filed with your U.S. tax return. Keep meticulous records of all transactions. For OPT workers from Niger, it is also wise to stay informed about any changes in U.S. banking regulations or your own immigration status that might affect your account. Consider consulting with a tax professional specializing in non-resident U.S. taxation to ensure all your financial activities are compliant. If you are still in the process of obtaining your ITIN or EIN, completing these steps first can significantly facilitate your banking application. You can review itin.net's Banking Setup services or contact us for personalized assistance with your U.S. banking needs.

Practical tips

- Ensure your passport is valid for at least six months beyond your application date to avoid issues with identification verification.

- Use the exact same legal name across all your applications, including your bank account, ITIN application (if applicable), and any employment documents.

- If applying for a business account, secure your EIN before starting the bank application process to prevent delays.

- Have a verifiable U.S. physical address ready, as most banks require this for account statements and card delivery.

- Research and choose a bank or fintech provider known for accommodating non-residents; avoid applying to major banks that typically decline international applicants.

Frequently asked questions

Can I open a U.S. bank account from Niger without traveling to the U.S.?

Yes, it is possible to open a U.S. bank account remotely from Niger. Many fintech companies and some traditional banks offer online application processes for non-residents. However, you will typically need a U.S. physical address for account statements and debit card delivery.

Do I need an ITIN or SSN to open a U.S. bank account?

While an ITIN or SSN can sometimes help, it is not always strictly required for opening a U.S. bank account as an OPT worker. Many institutions primarily rely on your passport and other identification. However, having an ITIN or SSN can expedite the process and is often necessary for tax-related matters.

What is the difference between a personal and business U.S. bank account for OPT workers?

A personal account is for individual transactions, while a business account is for business-related income and expenses. As an OPT worker, you might need a business account if you are freelancing or operating a side business. Business accounts typically require an EIN and business formation documents.

How long does it typically take to get a U.S. bank account approved?

The typical timeline for opening a U.S. bank account remotely for non-residents is 5–10 business days from the time of application submission and verification. This can vary based on the institution and the completeness of your documentation.

Can my employer in the U.S. help me open a bank account?

Your U.S. employer can often provide guidance and confirm the specific bank they use for payroll. They may also be able to provide a letter of employment, which can be helpful documentation. However, the application process itself is typically completed by you directly with the financial institution.

What if I don't have a U.S. physical address yet?

This is a common challenge. Some services offer mail forwarding or virtual mailbox solutions that can provide a U.S. address for banking purposes. However, verify with the bank if they accept such addresses, as some require a verifiable residential or business location.