Why Costa Rican Stock Investors Need a U.S. Bank Account

Stock investors based in Costa Rica face unique hurdles when managing U.S. equities. Primarily, many U.S. brokerage platforms and investment services require a U.S. bank account for account funding and withdrawals. This is often a standard Know Your Customer (KYC) and Anti-Money Laundering (AML) requirement, ensuring compliance with U.S. financial regulations. Without a U.S. bank account, you may be unable to open accounts with certain brokers, transfer funds efficiently, or receive dividend payments without significant currency conversion fees and delays. The absence of a U.S. banking relationship can create a barrier to entry or add considerable friction to your investment activities in the U.S. market. This is particularly true if you plan to trade actively or manage a substantial portfolio, where seamless and cost-effective fund movement is essential for timely execution of trades and reinvestment strategies. The U.S. market offers a vast array of investment opportunities, and a U.S. bank account is often the key to unlocking full participation for international investors.

Eligibility and Triggers for a U.S. Bank Account

A U.S. bank account becomes necessary for Costa Rican stock investors primarily when U.S. brokerage firms or investment platforms mandate it for account setup and transactions. Many popular platforms, such as Interactive Brokers, Charles Schwab International, and others catering to international clients, require U.S. dollar accounts for direct fund transfers. These institutions often have stringent compliance policies that favor U.S.-domiciled bank accounts for ease of verification and regulatory adherence. Furthermore, if you are receiving substantial dividend income from U.S. stocks, having a U.S. bank account can simplify the process of managing these funds and potentially reduce currency exchange costs. While some platforms might allow international wire transfers from Costa Rican banks, the associated fees, exchange rate markups, and longer processing times can be disadvantageous. For investors actively trading or managing significant assets, the efficiency and cost savings offered by a U.S. bank account are compelling reasons to pursue one. The trigger is often the account opening procedure of your chosen brokerage or investment service.

Required Documents for Non-Residents

Opening a U.S. bank account remotely as a non-resident requires specific documentation to satisfy bank and regulatory requirements. You will typically need a valid passport, which serves as your primary identification. Proof of residential address in Costa Rica is also mandatory; this can be a utility bill, bank statement, or government-issued document showing your name and address. If you are opening a business account, you will need documents related to your U.S. business entity, such as an EIN confirmation letter (Form CP-575) obtained from the IRS, and formation documents like Articles of Organization or Incorporation. Some banks may also request a U.S. physical address, which can often be satisfied through a registered agent service if you have formed a U.S. entity. The exact list of documents can vary between financial institutions, but these are the common requirements. Ensure all documents are clear, legible, and translated if not originally in English. The process involves a bank-specific application, not a federal form, focusing on KYC/AML compliance.

The Remote Application Process and Timeline

The process for opening a U.S. bank account remotely typically begins with selecting a bank or fintech provider that accepts non-resident applicants. Once you have chosen a provider, you will complete their online application form. This application will ask for personal details, information about your investment activities, and the documents previously mentioned. After submitting your application and supporting documents, the bank's compliance team will review them. This review stage can take several business days, as they verify your identity and assess your risk profile. If the application is approved, the bank will proceed with account opening. You will then receive your account details, and a debit card will be mailed to your address in Costa Rica. The entire process, from application submission to receiving your active debit card, generally takes between 5–10 business days. Some fintech solutions might offer faster activation, while traditional banks might have slightly longer review periods. Promptly providing all requested documentation can help expedite this timeline.

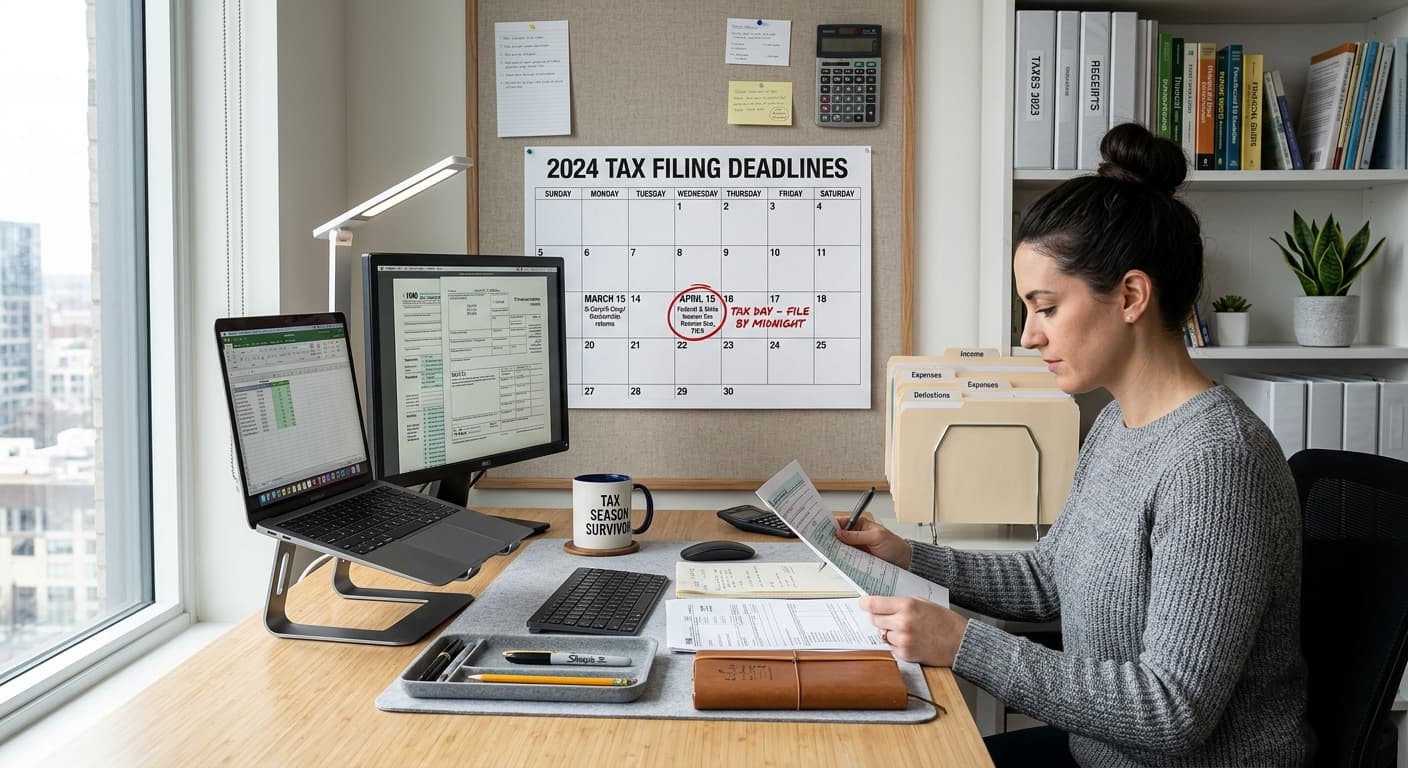

Common Mistakes for Costa Rican Stock Investors

Costa Rican stock investors often encounter specific pitfalls when applying for a U.S. bank account. A frequent error is attempting to open an account with traditional U.S. national banks, most of which decline non-resident applicants outright. It is crucial to target banks and fintechs that explicitly cater to international clients. Another common mistake is failing to provide complete or accurate documentation. For business accounts, neglecting to obtain an EIN or submitting incorrect formation documents can lead to rejection. Investors sometimes overlook the need for a U.S. physical address, which can be a requirement for some banks and is often fulfilled through a registered agent if you have a U.S. LLC. Ensure your application clearly states your purpose for the U.S. bank account, such as facilitating U.S. stock investments, which aligns with the services offered by providers like Mercury or Relay. Misunderstanding the application requirements or choosing the wrong financial institution are the most common reasons for delays or denials.

The Certified Acceptance Agent (CAA) Advantage

When applying for an ITIN, a Certified Acceptance Agent (CAA) like itin.net plays a crucial role in verifying your identity documents, simplifying the process. While a CAA is primarily involved in ITIN applications, their expertise in IRS procedures and documentation requirements indirectly benefits U.S. bank account opening. By successfully obtaining an ITIN through a CAA, you streamline the process of meeting identification requirements that might be needed for certain financial services or investment accounts. The CAA acts as a trusted intermediary, reducing the burden on you to send original identification documents to the IRS. This established process of identity verification through a CAA can sometimes be referenced or provide a level of assurance during financial institution applications, although direct bank requirements still apply. Using a CAA ensures that your identification documents are correctly certified, which is a critical step for any application involving the IRS or financial institutions that rely on verified identities. This specialized service is part of the broader support itin.net offers to individuals needing to engage with U.S. financial and tax systems.

Next Steps for U.S. Bank Account Holders

With your U.S. bank account established, you are well-positioned to enhance your stock investing activities. You can now seamlessly fund your U.S. brokerage accounts, receive dividends directly, and execute trades with greater efficiency. Ensure you keep your banking information updated with your brokerage and any other U.S. financial services you use. If you plan to expand your U.S. business activities or require more complex financial structures, consider consulting with a professional regarding U.S. LLC formation or other entity types. For those who may need an ITIN for tax purposes related to their U.S. investments or income, exploring the application process is the next logical step. Review the specific banking packages available at itin.net or contact us directly to discuss your needs and how we can assist you in setting up your U.S. financial infrastructure.

Practical tips

- Use the same legal name across all applications – passport, bank forms, and any prior IRS correspondence. Mismatched names are a primary reason for application delays or rejections.

- Target U.S. fintech companies like Mercury, Relay, or Brex, or specialized international banks, as most major U.S. national banks do not accept non-resident remote applications.

- For business accounts, secure your EIN first. Many U.S. banks require an EIN and formation documents (like Articles of Organization) before they will open an account for a non-resident entity.

- Clearly state the purpose of your U.S. bank account in the application. Mentioning stock investing and managing U.S. dividends demonstrates a legitimate need that aligns with services offered by international-friendly banks.

- Anticipate a verification process that may involve a video call or additional documentation requests. Respond promptly to any communication from the bank to avoid unnecessary delays in account activation.

Frequently asked questions

Can I open a U.S. bank account from Costa Rica without visiting the U.S.?

Yes, it is possible to open a U.S. bank account remotely from Costa Rica. Many U.S. banks and fintech providers have online application processes designed for non-residents. You will need to provide specific documentation for verification, but physical presence in the U.S. is generally not required.

Do I need an ITIN to open a U.S. bank account?

An ITIN is not always required to open a U.S. bank account, especially for personal accounts. However, some banks might request it, particularly for business accounts or if you intend to invest in U.S. securities that require tax reporting. Having an ITIN can sometimes expedite the process and is often necessary for tax compliance related to U.S. income.

What are the typical fees associated with a U.S. bank account for non-residents?

Fees vary by institution. Common fees include monthly maintenance fees (often waived if minimum balance requirements are met), wire transfer fees (both domestic and international), foreign transaction fees, and ATM withdrawal fees. Some fintech accounts may offer lower or no monthly fees but could have other transaction-based charges.

How long does it take to receive my U.S. bank account debit card in Costa Rica?

Once your U.S. bank account is approved, the debit card is typically mailed to your address. Delivery to Costa Rica can take anywhere from 5 to 15 business days, depending on the shipping method used by the bank and local postal services.

Can I use my U.S. bank account to directly fund a U.S. stock trading account?

Yes, this is one of the primary benefits. A U.S. bank account allows for direct electronic fund transfers (ACH) or wire transfers to U.S. brokerage accounts, which is usually faster and less expensive than international transfers from a Costa Rican bank.

What if my U.S. brokerage account requires an ITIN or SSN, and I only have an ITIN?

If your brokerage requires an SSN and you only have an ITIN, you may need to explicitly inform them that you are a non-resident alien using an ITIN for tax reporting purposes. Some platforms have specific procedures for ITIN holders. If they are unfamiliar with ITINs, you may need to seek a different brokerage or consult with a tax professional. Having an ITIN allows you to comply with U.S. tax reporting requirements on investment income.